Results reflect consistent execution of the Company’s investment-led

customer-centric strategy

The Company reiterates all full-year 2026 and multi-year financial guidance

and capital return plans

Download release (PDF)

Download 1Q2026 Earnings Highlights Document

AT&T Inc. (NYSE: T) reported first-quarter results, achieving its fastest-ever year-over-year organic growth in its advanced connectivity convergence rate, with nearly 45%1 of advanced home internet subscribers also choosing AT&T wireless. Customers are increasingly purchasing their internet and wireless together from AT&T, highlighting the strength of the Company’s differentiated, investment-led strategy to drive converged advanced connectivity at scale.

“We saw our best first quarter ever for Advanced Connectivity internet customer net additions, demonstrating the solid foundation of assets we have built,” said John Stankey, AT&T Chairman and CEO. “We’re uniquely positioned to deliver more of what customers want — fiber and 5G all from one provider on the nation’s largest advanced converged network, backed by the AT&T Guarantee. The actions we’ve taken this quarter are evidence of how we are improving the customer value proposition, scaling faster, and accelerating growth.”

Note: With the closing of the acquisition of substantially all of Lumen’s Mass Markets fiber business on February 2, 2026, the fiber customer relationships were retained by AT&T and are included in the Company’s first-quarter results, unless otherwise indicated. The acquired fiber network assets, including certain fiber network build capabilities, were placed in a wholly owned subsidiary, of which AT&T plans to sell a controlling interest to an equity partner that will co-invest in the ongoing business. As such, the subsidiary is classified as held-for-sale and reflected as discontinued operations.

First-Quarter Consolidated Results

- Revenues totaled $31.5 billion, up 2.9% from the year-ago quarter

- Diluted EPS from continuing operations was $0.54, versus $0.61 in the year-ago quarter; adjusted EPS* was $0.57, versus $0.51 in the year-ago quarter

- Operating income was $6.7 billion; adjusted operating income* was $6.9 billion

- Income from continuing operations was $4.2 billion; adjusted EBITDA* of $11.8 billion

- Cash from operating activities from continuing operations was $7.6 billion, versus $9.0 billion in the year-ago quarter, which included $1.4 billion from the DIRECTV investment

- Capital expenditures related to continuing operations were $4.9 billion; capital investment* was $5.1 billion

- Free cash flow* was $2.5 billion, versus $3.1 billion in the year-ago quarter, reflecting higher capital investment as the Company accelerates the pace of its fiber deployment

First-Quarter Highlights

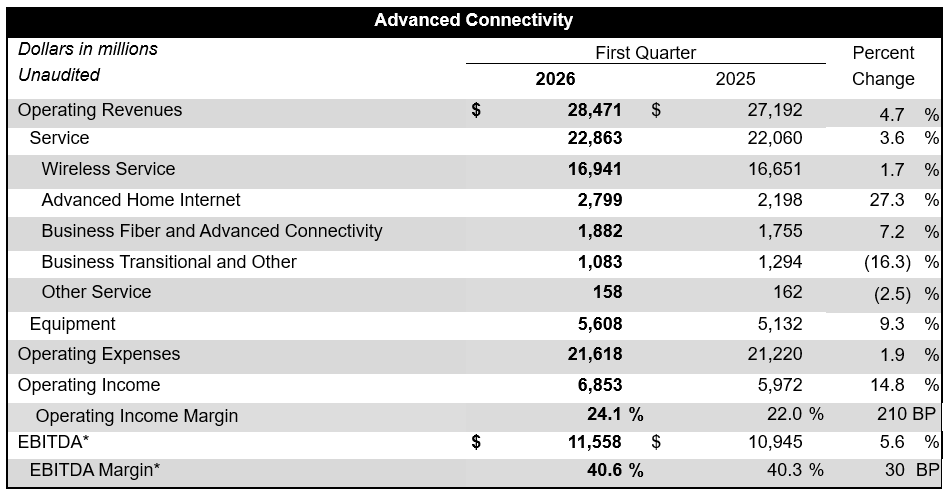

- Advanced Connectivity service revenue of $22.9 billion, up 3.6% year over year

- Advanced Connectivity operating income of $6.9 billion, up 14.8% year over year with EBITDA* of $11.6 billion, up 5.6%

- 42% of households with AT&T’s advanced home internet services also chose AT&T wireless; this approaches 45% when excluding the impact of fiber customers acquired during the quarter, up over 3 percentage points year over year, representing the fastest-ever reported organic growth in the advanced home internet convergence rate

- 584,000 total consumer and business Advanced Connectivity internet net adds, including 292,000 fiber and 292,000 fixed wireless

- 512,000 consumer advanced home internet net adds, including 273,000 AT&T Fiber2 and 239,000 AT&T Internet Air

- 294,000 postpaid phone net adds with postpaid phone churn of 0.89%

- Over 37 million total consumer and business locations reached with fiber3, including more than 4 million acquired from Lumen during the first quarter; the Company remains on track to reach over 40 million total fiber locations by the end of 2026 and more than 60 million by the end of 2030

- Repurchased approximately $2.3 billion in common shares under the 2024 authorization

Outlook and Capital Allocation Plan

AT&T maintains the long-term outlook and capital allocation plans provided with its fourth-quarter 2025 results. This includes the Company’s outlook for improved growth in adjusted EBITDA* and adjusted EPS* and higher free cash flow* through 2028, its plans to return $45 billion+ to shareholders during 2026-2028 through dividends and share repurchases, and an expectation that its net debt-to-adjusted EBITDA ratio* will return to a level consistent with its target in the 2.5x range within approximately three years following the closing of its transaction with EchoStar.

For 2026, AT&T continues to expect4:

- Service revenue growth in the low-single-digit range, including Advanced Connectivity service revenue growth of 5%+ and a decline in Legacy service revenue of 20%+

- Adjusted EBITDA* growth in the 3% to 4% range, including Advanced Connectivity EBITDA* growth of 6%+

- Adjusted EPS* of $2.25 to $2.35

- Capital investment* in the $23 billion to $24 billion range

- Free cash flow* of $18 billion+, including cash taxes of $1.0 billion to $1.5 billion and cash contributions to its employee pension plan of approximately $350 million

- Consistent capital returns, including plans to maintain its current annualized common stock dividend of $1.11 per share and share repurchases of approximately $8 billion

Note: AT&T’s first-quarter 2026 earnings conference call will be webcast at 8:30 a.m. ET on Wednesday, April 22, 2026. The webcast and related materials, including financial highlights, will be available at investors.att.com.

Consolidated Financial Results

- Revenues for the first quarter totaled $31.5 billion, versus $30.6 billion in the year-ago quarter, up 2.9%. This was largely due to growth in Advanced Connectivity wireless and fiber revenues, including two months of impact from the customers acquired from the Lumen transaction. Operating revenues in Mexico were also higher due to favorable foreign exchange impacts during the first quarter of 2026. Offsetting these increases were lower Legacy revenues from lower demand for services as the Company continues to decommission its copper-based network.

- Operating expenses were $24.8 billion, a slight decline versus $24.9 billion in the year-ago quarter. Operating expenses decreased primarily due to lower depreciation expense from fully depreciated legacy assets, partially offset by ongoing capital spending for strategic initiatives. Also contributing to the decline were higher restructuring charges in the year-ago quarter, cost reductions from transformation initiatives and lower content licensing fees. These decreases were largely offset by higher wireless sales volumes, which drove higher equipment, selling, and bad debt expenses, higher network costs that included vendor credits in the year-ago quarter, and incremental customer costs related to the acquired Mass Markets fiber business.

- Operating income was $6.7 billion, versus $5.8 billion in the year-ago quarter. When adjusting for certain items, adjusted operating income* was $6.9 billion, versus $6.4 billion in the year-ago quarter.

- Income from continuing operations was $4.2 billion, versus $4.7 billion in the year-ago quarter, which included equity in net income of DIRECTV.

- Income from continuing operations attributable to common stock was $3.8 billion, versus $4.4 billion in the year-ago quarter. Earnings per diluted common share from continuing operations was $0.54, versus $0.61 in the year-ago quarter. Adjusting for $0.03, which includes acquisition-related amortization and other items, adjusted earnings per diluted common share* was $0.57, versus $0.51 in the year-ago quarter.

- Adjusted EBITDA* was $11.8 billion, versus $11.5 billion in the year-ago quarter.

- Cash from operating activities from continuing operations was $7.6 billion, versus $9.0 billion in the year-ago quarter, which included $1.4 billion from the DIRECTV investment.

- Capital expenditures related to continuing operations were $4.9 billion, compared to $4.3 billion in the year-ago quarter. Capital investment* totaled $5.1 billion, versus $4.5 billion in the year-ago quarter. Cash payments for vendor financing totaled $0.2 billion, consistent with the year-ago quarter.

- Free cash flow* was $2.5 billion, versus $3.1 billion in the year-ago quarter.

- Total debt was $138.4 billion at the end of the first quarter, and net debt* was $126.4 billion.

Segment Results

Effective with the Company’s first-quarter 2026 reporting, AT&T has revised its operating segments to reflect the evolution of its business model to focus on delivering converged advanced connectivity services.

Advanced Connectivity service revenues grew 3.6% year over year, driving growth in operating income of 14.8% and EBITDA* of 5.6%. Internet net adds were 584,000 — comprised of 292,000 fiber and 292,000 fixed wireless — and postpaid phone net adds were 294,000.

Advanced Connectivity segment revenues grew 4.7% year over year, driven by service revenue growth of 3.6% and increased equipment revenues of 9.3% from higher wireless device sales volumes. Wireless service revenue increased due to growth in retail wireless subscribers in underpenetrated categories and converged accounts, partially offset by the amortization of promotional activity. Advanced home internet revenue growth, which included two months of impact from the acquired Mass Markets fiber business, reflects increases in fiber and AT&T Internet Air revenues. Business fiber and advanced connectivity revenues increased largely due to higher fiber and fixed wireless revenues. Business transitional and other revenues decreased partly due to lower demand for virtual private network and wholesale services.

Operating expenses were up 1.9% year over year, driven by higher wireless sales volumes, which drove higher wireless equipment, selling, and bad debt expenses. The increase also included higher network costs that included vendor credits in the year-ago quarter, and higher incremental customer costs related to the acquired Mass Markets fiber business, which were partially offset by cost reductions from transformation initiatives and lower content licensing fees. Depreciation expense was lower due to fully depreciated legacy assets, partially offset by ongoing capital spending for strategic initiatives.

Operating income was $6.9 billion, up 14.8% year over year. EBITDA* was $11.6 billion, up $613 million year over year.

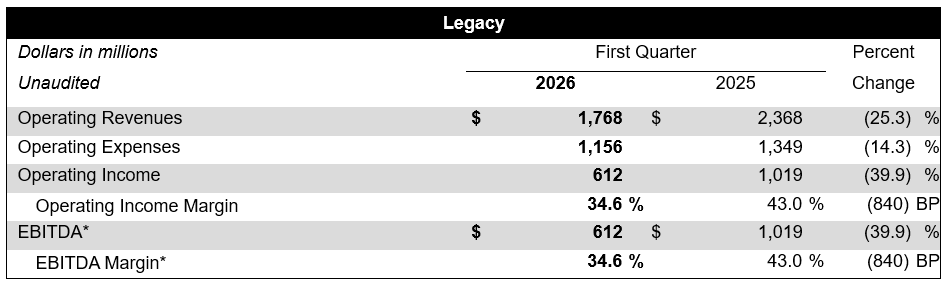

Legacy revenues continued to decline year over year in line with AT&T’s goal to power down and stop providing service over the large majority of its domestic copper-based network by the end of 2029.

Legacy segment revenues were down 25.3% year over year, primarily due to lower demand for services as the Company continues to decommission its copper-based network. Operating expenses, which represent direct operating costs, were $1.2 billion, down 14.3% year over year. Expense declines were primarily driven by lower personnel and other costs resulting from the decommissioning of the copper-based network and lower fulfillment cost amortization, which were partially offset by vendor credits in the year-ago quarter. Operating income and EBITDA* were $612 million, down $407 million year over year.

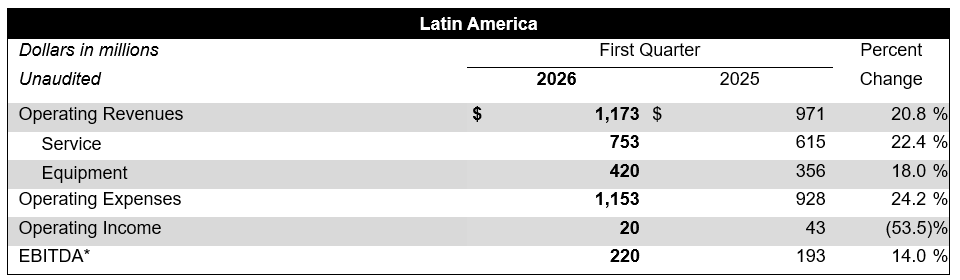

Latin America segment revenues were up 20.8% year over year, driven by favorable foreign exchange impacts as well as growth in subscribers and increased equipment sales. Operating expenses were up 24.2% year over year due to unfavorable foreign exchange rates, increased sales volumes that resulted in higher equipment costs and bad debt expense, and higher depreciation expense. Operating income was $20 million, down $23 million year over year. EBITDA* was $220 million, up $27 million year over year.

PR Archives: Latest, By Company, By Date